Example. Son continues to attend daycare after turning 3

A taxpayer started working as a temporary permanent worker in January 2021. In 2021 he worked from January 8 to June 24 and from September 7 until the end of the year.

Has a son born on 02/11/2018. He attended daycare between January and July 2021, paying a total of €3,500 (€500/month).

In her 2021 Income Tax return, the taxpayer applied the maximum amount that corresponded to her from the maternity deduction and the increase for childcare expenses in accordance with the regulations in force at that time.

Analyze the effect of the extension of the maternity deduction to the new circumstances for the year 2021 knowing that the amount of the total contributions and fees (of the worker and the company) is as follows: €200 for the months in which he/she is working and €110 in July and August.

Solution

- EXISTING SITUATION UNTIL 31/12/2022 (original regulations):

1.1. Maternity deduction in Income Tax 2021:

The requirements for carrying out an activity as a self-employed person or employed by another person with registration with Social Security and having a child under 3 years of age simultaneously apply exclusively in the month of January, given that the child turned 3 in February (the month in which the child turns 3 does not count since the month of birth does).

In the 2021 Income Tax Return, the maternity deduction was recorded for an amount of €100:

-

Maximum deduction originally possible: 1 month (January) x €100/month = €100.

-

Limit on contributions (those corresponding to the month of January, which is the month in which the child is less than 3 years old): 200 €. The limit does not operate.

-

Maternity deduction in Income Tax 2021 = €100.

1.2 Increase for childcare expenses in Income Tax 2021:

In the year in which the child turns 3, as is the case here, the increase may be applied to the nursery expenses paid after reaching that age until the month before the second cycle of early childhood education can begin, that is, until August included.

In this way, the increase is calculated proportionally to the number of months in which the requirements for its application are met. Therefore, for each month that you meet these requirements, you will receive an increase of €83.33 (€1,000 / 12 months). In this case, the child has attended daycare for 7 months, of which the mother has been active for 6 (between January and June, both included). Therefore:

-

Maximum possible deduction amount originally = 6 months (January to June) x €83.33/month = €500.

-

With the limit of the lesser of the following amounts:

-

Contributions accrued up to the month prior to the month in which the child can begin the second cycle of early childhood education, that is, from January to August inclusive = €1,420.

-

Quantities satisfied: 3,500 €.

-

The limits do not apply as they are higher than the maximum amount to be obtained.

-

-

Increase for expenses in authorized nurseries or early childhood education centers applied in Income 2021: 500 €.

-

-

EXTENSION IN INCOME 2022 OF THE MATERNITY DEDUCTION AND THE INCREASE IN DAYCARE EXPENSES YEAR 2021 .

2.1 Extension in Income Tax 2022 of the Maternity Deduction 2021:

Since the child turned 3 in February and the taxpayer has already obtained the maximum amount of the maternity deduction that could correspond to her, the extension is not applicable.

2.2. Extension in Income Tax 2022 of the Deduction for increased childcare expenses 2021:

With the extension to the new circumstances that includes the case of fixed-discontinuous workers who are in a period of productive inactivity, in the 2022 Income Tax return they will be able to include the deduction for the month of July in which the child went to daycare and which was not included in the 2021 Income Tax return as this right does not exist.

In this way, instead of 6 months, you will be entitled to 7.

-

New maximum possible deduction amount = 7 months (January to July) x €83.33/month = €583.33.

-

With the limit of the lesser of the following amounts:

-

Contributions accrued up to the month prior to the month in which the child can begin the second cycle of early childhood education, that is, from January to August inclusive = €1,420.

-

Quantities satisfied: 3,500 €.

The limits do not apply as they are higher than the maximum amount to be obtained.

-

-

New amount of the increase in the deduction for childcare expenses: 583,33 €.

-

Amount applied in 2021: 500 €.

-

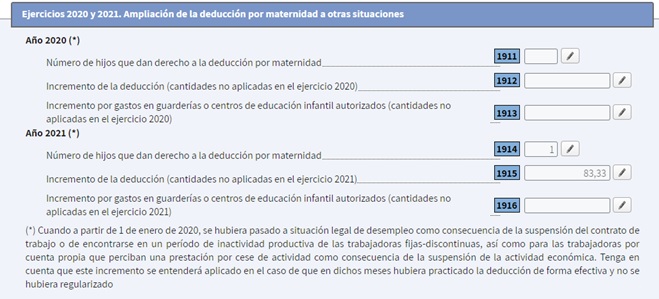

Extension of the deduction for the increase in expenses in authorized nurseries or early childhood education centers in 2021 to be received in Income Tax 2022: 583.33 – 500 = €83.33.

This amount is the one that must appear in box of the 2022 Income Tax Return “Increase for expenses in authorized nurseries or early childhood education centers (amounts not applied in the 2021 fiscal year)”:

-